Note: The following is written for those who live in non– community property or non–marital property states. If you live in Alaska, Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, or Wisconsin the outcomes may differ from the following examples.

The beneficiary designation is often the most misunderstood and underappreciated tool in the estate planning toolbox. Let’s see how you would respond to the following questions:

True or False . . .

- I recently updated my “will,” so I don’t need to bother with IRA beneficiary designations.

- I recently updated my “trust,” so I don’t need to bother with IRA beneficiary designations.

- If I forget to change the primary beneficiary designation for my IRA after I remarry and it still lists my ex-spouse when I pass away, my IRA

custodian has the responsibility to overlook my “lapse” and direct the proceeds in a manner that is logical. - By designating “my estate” as the primary beneficiary of my IRA, I provide more flexibility for how the account will be distributed when I pass away.

- Designating my minor children is a good idea as long as they are contingent beneficiaries.

And the Answers Are . . .

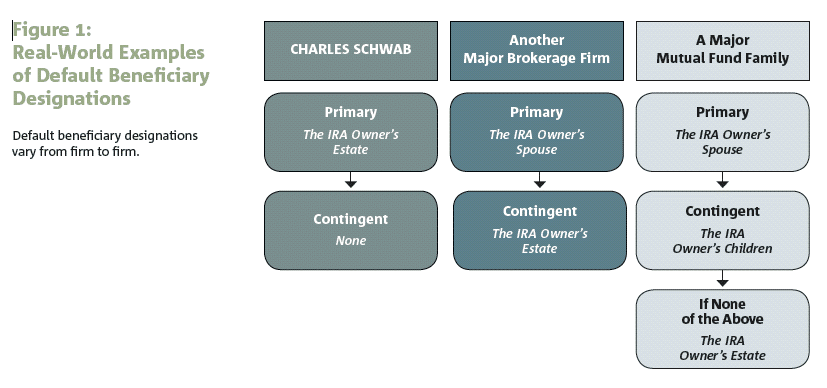

- False. Many IRA owners believe that the instructions they provide in their will override the beneficiary designation of their IRA. In fact, your IRA beneficiary designation overrides the instructions in your will. All IRA custodians have a default beneficiary designation ready to step in if you do not name a beneficiary, but the default can differ from custodian to custodian. Figure 1 (below) compares a few actual default beneficiary designations.

If your IRA beneficiary defaults to your estate, please read #4 for “the rest of the story.”

- False. In an effort to save space and not repeat myself, read the above answer and replace the word “will” with the word “trust.”

- Sorry Spock, this too is false. Even if it seems logical, the IRA custodian must follow the beneficiary designation and, in this case, distribute the IRA to the ex-spouse. What can cause confusion for the IRA owner is that the rules are different for some employer-sponsored retirement plans such as 401(k)s because they fall under federal law, unlike IRAs, which fall under state law. Federal law requires a spouse to sign a waiver if the 401k owner designates anyone other than his or her spouse (or in addition to the spouse) as primary beneficiary. In our example, if the current spouse did not sign a waiver, the proceeds of the 401k would go to him or her.

- False. By designating “my estate,” an IRA owner can remove some powerful estate planning tools from the toolbox with a result similar to designating no beneficiary at all. The consequences include:• A loss of the “spousal continuation” provision

• A loss of the “stretch IRA” option (more about this in a future newsletter)

• Fewer distribution options and thus potentially higher income tax rates

• The IRA being subject to probate — a costly, time-consuming, and public process - False. A minor cannot inherit an IRA in his or her name. If a minor is designated as a beneficiary of an IRA and the IRA owner passes away without setting up a trust or leaving clear instructions about custodianship, anyone, including a parent, seeking custodianship for the heir’s IRA may have to go to court to be appointed. Many IRA custodians will default to the minor’s legal guardian which may or may not be what the IRA owner intended.

- A relatively simple solution is the Unified Transfer to Minor Account (UTMA), in some states called Unified Gift to Minor Account (UGMA). The beneficiary designation would read something like this: “25% to Robert Smith III, but, if a minor, the beneficiary is Robert Smith II custodian for Robert Smith III under the UTMA of [name of state].” The downside to UTMAs is that the child will receive the account when they reach age of majority, typically age 18 or 21 (depending on the state).A not-so-simple solution is to identify a trust as a beneficiary. This can offer some unique “control from the grave” planning opportunities that some IRA owners appreciate. If you name a trust as your IRA beneficiary, the trust has to be well drafted or it can cause more problems than it is worth. This would be an appropriate time to seek the advice of an estate planning attorney.

In Closing . . .

It is not my intent to make light of beneficiary designations by using a game show approach for this article. It is my hope that I would capture your attention enough to have you scratch your head and think about your beneficiary designations. When done correctly, they can be an inexpensive yet powerful estate planning tool. When done poorly, they can be a disaster waiting to happen. Unfortunately, when the disaster does happen, the IRA owner is not around to help clean up the mess.