The investment strategy I am currently pursuing on your behalf is based on two questions:

What is the probable financial outcome given both America’s and the world’s handling of the Covid-19 pandemic?

How attractive are investment opportunities within that framework?

As of June 30, 2020 (if MCS clients’ investments were treated as one large portfolio including their cash), on average clients lost 0.25%1, after this year. For comparison purposes, the S&P 500 Total Return Stock Index (S&P 500) fell 3.1%, and the Barclays Aggregate Bond Index gained 6.1%. The range of MCS individual client returns was from a gain of 4.05% to a loss of 6.91%.

Clients with the lowest returns had higher overall allocations to equities because most of their investments were in a pension plan with low equity exposure (so their combined return was better than their non-qualified returns). Clients with the highest returns had exposure to select low-basis stocks that did well or had no equity exposure at all. Overall, MCS client returns were protected by the defensive posture of their portfolios. Short term bonds and low overall exposure to stocks meant that MCS clients remained steady while significant volatility swirled around stock and bond investors.

In last quarter’s newsletter, I talked about chaos. You may have heard the about the Butterfly Effect: by flapping its wings in the just right initial conditions, a butterfly’s slight disturbance of air can create a chain reaction resulting in a tornado. It’s a metaphor that has some basis in fact about the nature of chaotic systems. Small changes in initial conditions can lead to large scale events.

Well, we have just witnessed a Butterfly Effect. The butterfly was an alleged phony $20 bill and a refusal to give up a pack of cigarettes purchased with it. A reactive / escalating set of circumstances lead to the brutal, senseless death of George Floyd, followed by national and global chaos which continue reverberating at high levels of reactivity.

To make things worse, this historic movement for social change is happening smack dab in the middle of a pandemic. Not only has COVID-19 reasserted itself as we reopen, but a race relations crisis that was smoldering for decades has now burst into flame. This has led to a law enforcement crisis, in which people are now questioning whether the warrior police model is counterproductive in many situations. Add to that a contentious national election exacerbated by the collapse of trust among the American people. The ongoing pandemic, experimental policies from the Fed, and the increased odds of a Democratic win likely resulting in higher taxes: it appears there’s plenty of opportunity for more volatility ahead.

What follows is my assessment of our pandemic trajectory, economic trajectory, and the interplay between the two as expressed by the stock and bond markets. In addition, it is important to consider the potential impact of my assessment being wrong.

Below are tables I created as a tool to help me work through these complex issues, and I share them with you so you can see where I’m coming from as I consider the pandemic and the economy. I read a lot of articles from a wide variety of sources. If you have any insights, observations, or information you feel would be relevant, please send me an email.

Analysis

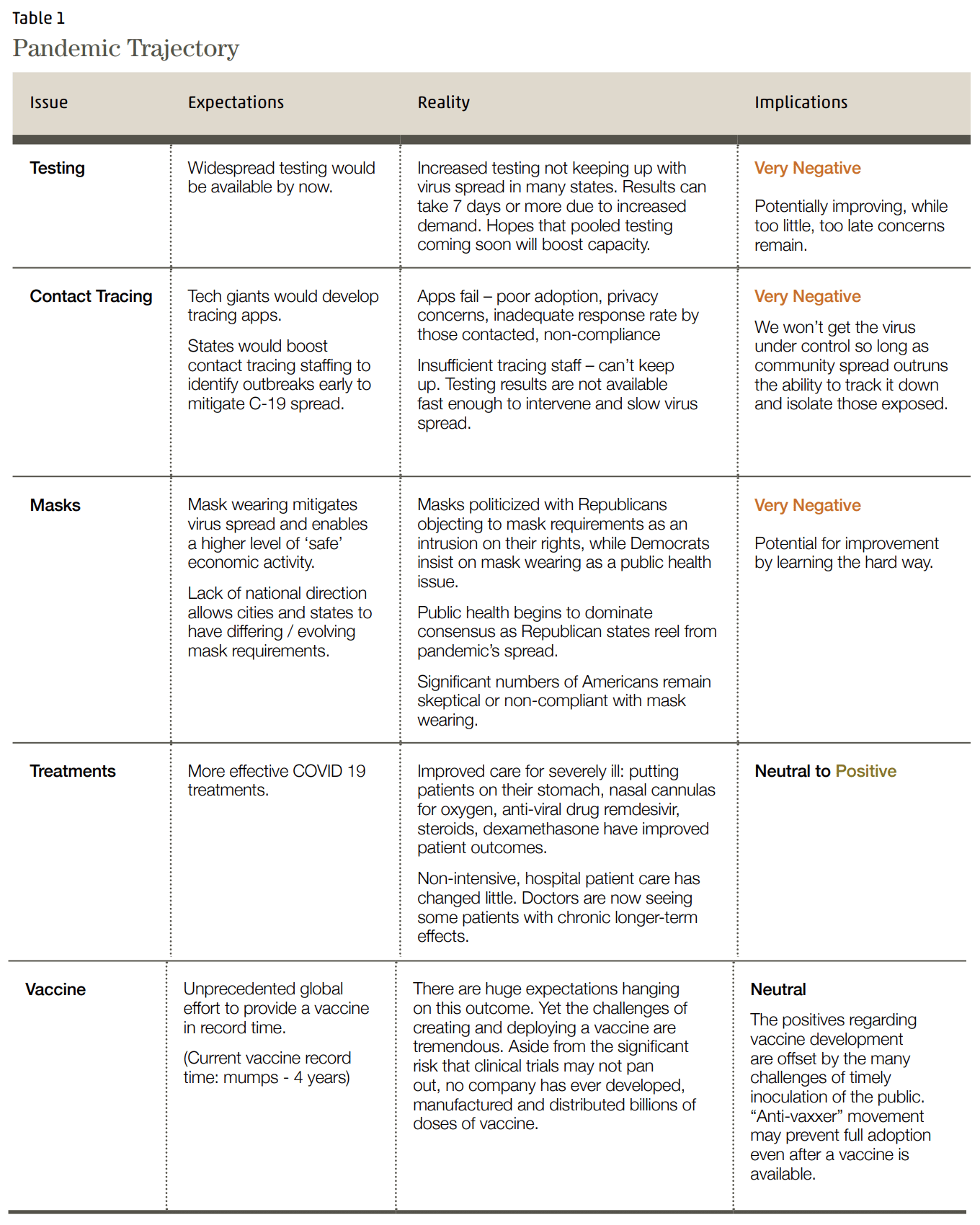

In the US, the virus is currently beating our ability to contain it. An effective, widely available vaccine is being touted as just around the corner. Yet, given the multitude of complexities in executing such a task, a vaccine introduction may look more like our inadequate efforts to implement widespread testing and contact tracing.

I expect a lot of consumer confusion about COVID-19 vaccines given the many trials and sped up development process. It will not take many reports of adverse outcomes to cool people on getting vaccinated, despite the expected benefits. Would it be surprising if “the government can’t tell me to wear a mask” folks morph into “the government can’t tell me to get shots” folks and join the “I don’t trust big pharma / anti-vaccine folks?”

If this sounds too pessimistic, consider the concerns raised in Journal of American Medical Association (JAMA) Viewpoint on May 30, 2020. “Adverse Consequences of Rushing a SARS-CoV-2 Vaccine: Implications for Public Trust2.” The article describes problems with the Salk polio vaccine in 1955:

As speed took precedence over caution, serious mistakes went unreported. One company, Cutter Laboratories, distributed a vaccine so contaminated with live poliovirus that 70,000 children who received that Vaccine developed muscle weakness, 164 were permanently paralyzed, and 10 died.

It goes on to discuss he 1976 swine flu vaccination program, saying:

Poorly conceived, the attempt to vaccinate the US population at breakneck speed failed in virtually every respect. Safety standards deteriorated as one manufacturer produced the incorrect strain. The vaccine tested poorly on children who, depending on the form of vaccine tested, either developed adverse reactions with high fevers and sore arms or did not mount an immune response at all. Reports emerged that the vaccine appeared to cause Guillain-Barré syndrome in a very small number of cases, a finding that remains controversial, but added to the early momentum of the antivaccine movement.

Other challenges to manufacturing a vaccine at an unprecedented scale include:

The world does not manufacture enough medical grade glass vials to meet the demand, especially if the vaccine requires a second booster shot, and

Vaccine nationalism, where it is every country for themselves. The first to tie up the supply chain resources wins: what you can’t develop at home, buy; what you can’t buy, steal.

From Lazard’s Global HealthCare Leaders Study3 released July 16, 2020:

Healthcare industry leaders’ single biggest concern is the availability of an effective vaccine to prevent infections. They are sober about the length of time it will likely take to develop widely available effective vaccines to bring the COVID-19 pandemic under control, and they expect this will not happen until well into 2021, if not later.

To summarize: efforts to develop vaccines will pay-off, but the timing is uncertain. The pandemic is creating breakthroughs and valuable lessons. Yet, it’s a very messy experiment on many levels and it would be naïve to assume the timing and consequences will be only positive for those involved.

Macro-Economic Analysis

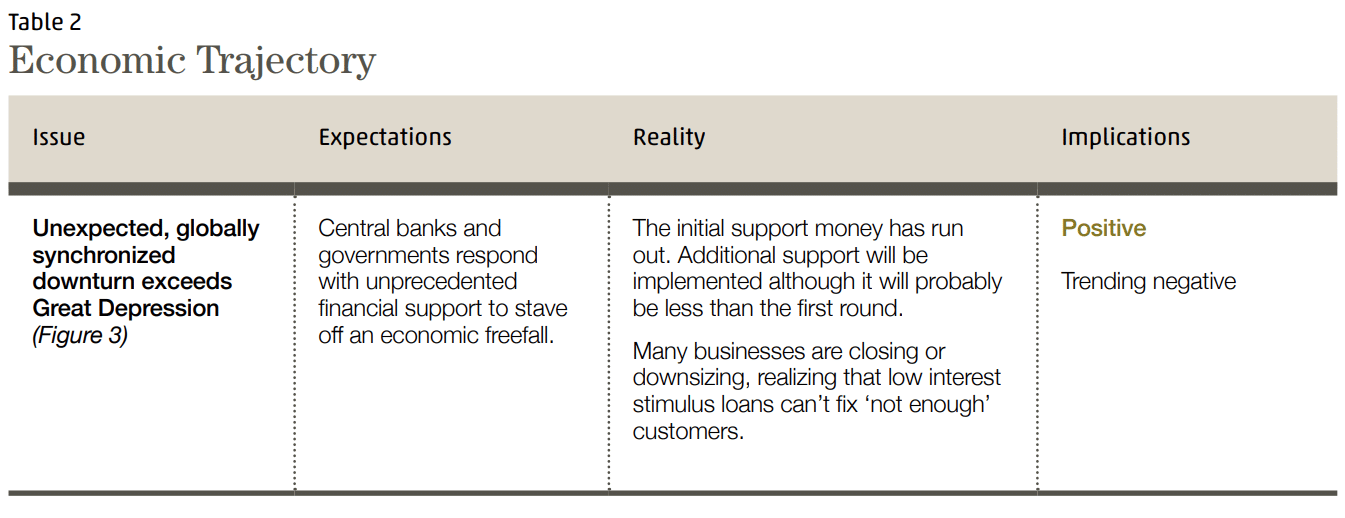

The global pandemic has had a crushing impact on the world economy. Pandemics, like other natural disasters, have varying economic impacts. Wall Street typically dismisses regional natural disasters because the impact on the national economy is muted. However, each disaster has a significant impact on the local economy. Areas hit by severe disasters do not quickly rebound to pre-disaster activity despite federal assistance. The global pandemic qualifies as a severe natural disaster in my mind, which implies a long, uneven global recovery.

Comments

A business and consumer insolvency crisis rapidly unfolded as the pandemic lead to lockdowns (insolvency means not having enough cash on hand to pay bills). The government responded by sending money to individuals and businesses with the hope of bridging the financial problems after lockdowns caused a ‘hard stop’ of economic activity. The hope was that the hard stop would be short lived, but the recovery has faltered as the reopening has created a surge in COVID-19 infections. Regardless of whether economic lockdowns are reinstated, many consumers will not return to their normal economic activity until they feel safe. Yet, safety from the virus may be an illusion. It may settle into humanity as a more deadly version of the flu, where an annual COVID-19 vaccine mitigates the healthcare impact but does not eliminate it.

A counterintuitive possibility is that a promised and ‘soon-to-arrive’ vaccine makes the global economy worse over the short run. A rational response to a soon-to-arrive vaccine for the wealthier over 55 year-olds, who make up a disproportionally large share of leisure consumption, is a self-imposed mini-lockdown while waiting for the miracle vaccine. Yet, it is not hard to imagine the vaccine’s ‘time to delivery’ encountering setbacks which delay the economic rebound.

The pandemic is an invisible tsunami washing over the world. A government cannot stop the destruction of a tsunami simply by offering money and loans to people and businesses in coastal towns. The post-tsunami cleanup takes years and the landscape is permanently altered.

Uncertainty is the Certainty

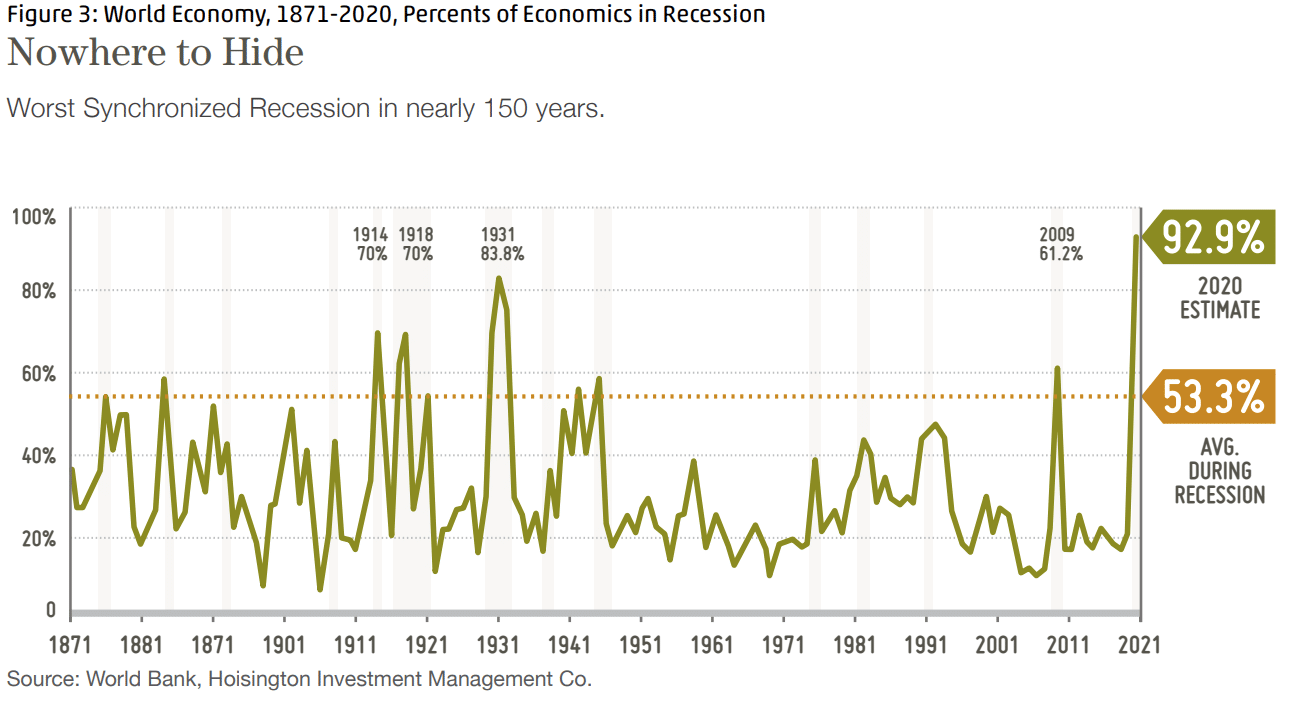

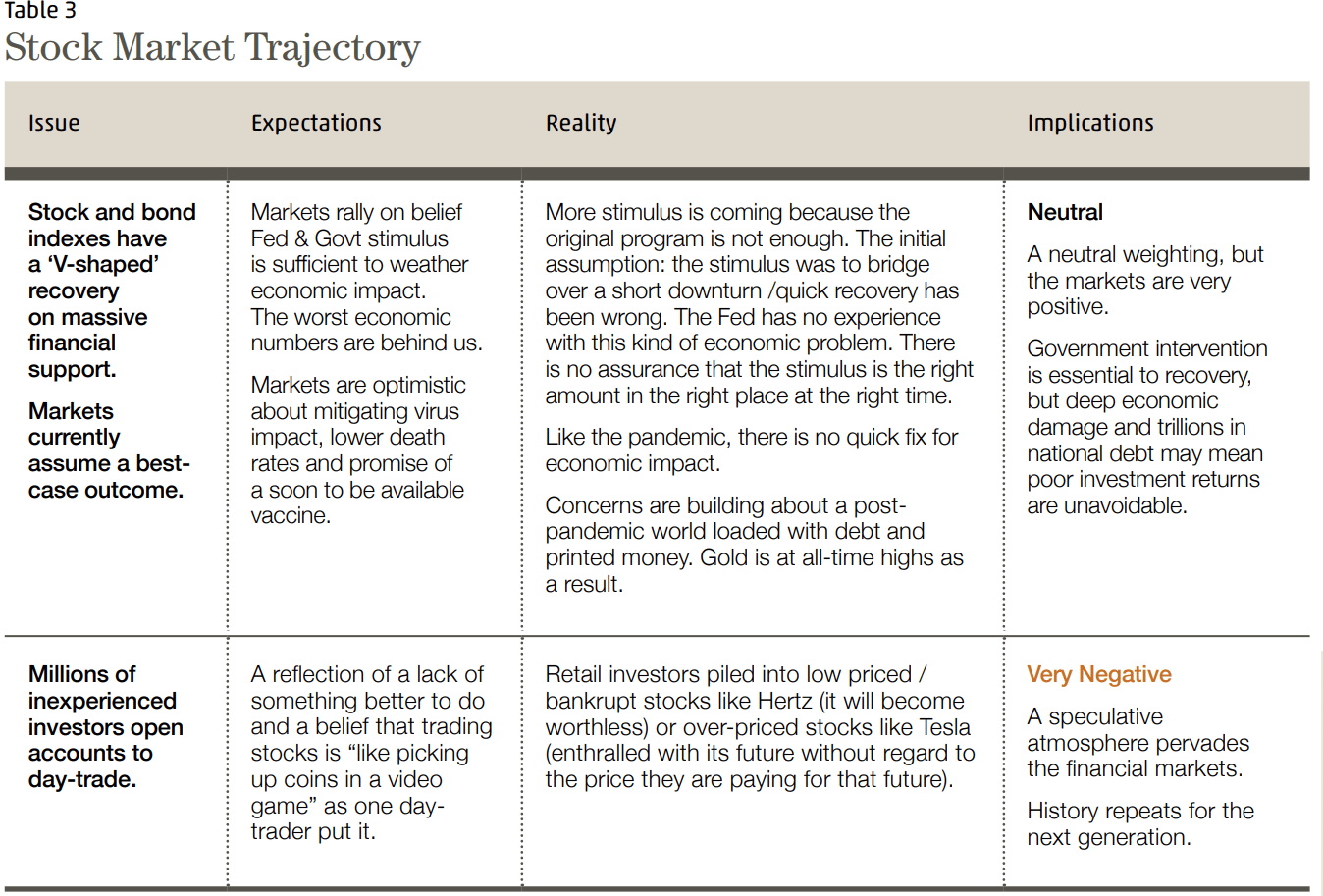

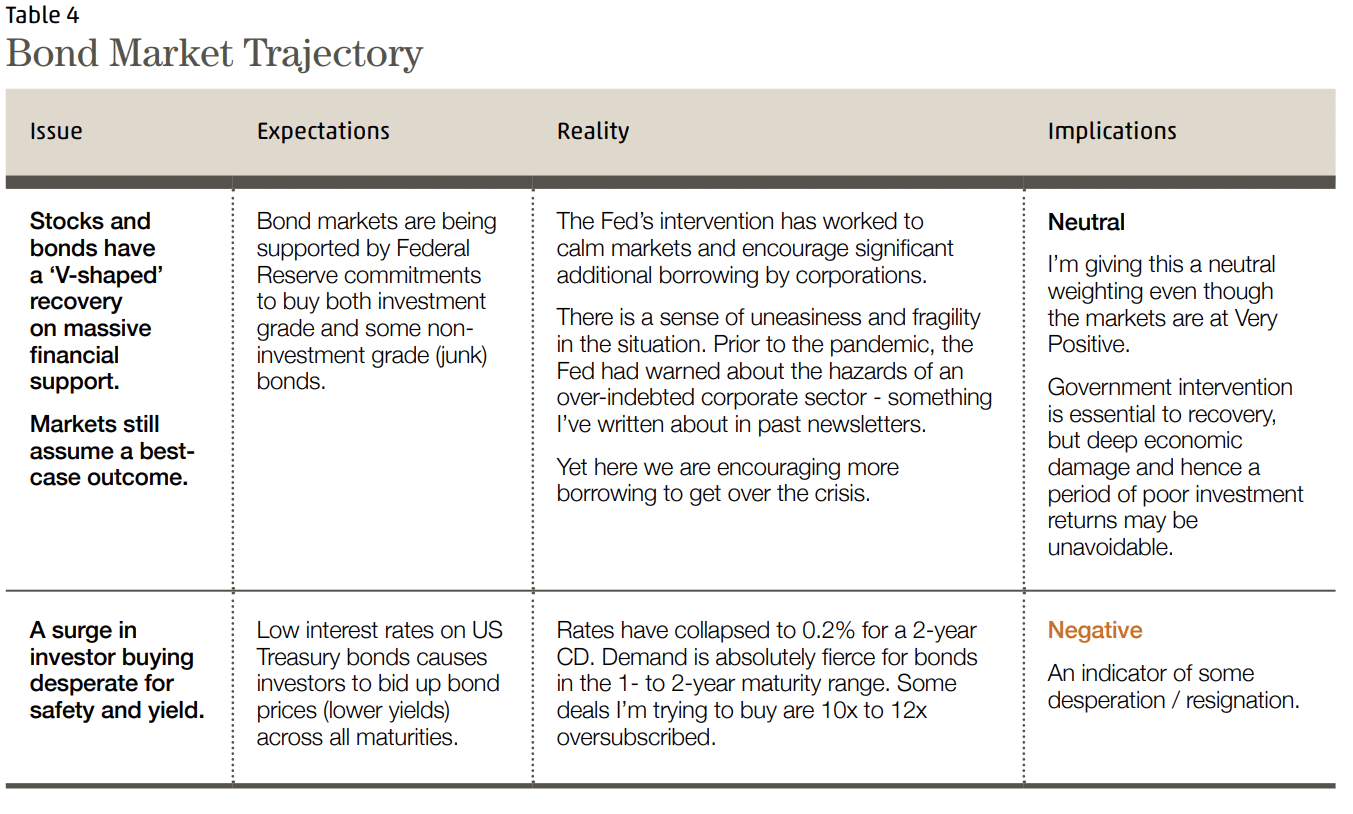

How have asset prices reacted to a global pandemic and the worst globally synchronized recession in 150 years?

Comments

Because of the unprecedented amount of government money thrown at both the economy and a vaccine, stock prices reflect expectations of a relatively short-lived recession. Frankly I don’t have faith that people who didn’t see the pandemic coming, and who are still learning in real time, will now clearly see how this ends. Of course, it will end, as all pandemics eventually do. The open question is what the US and global economy look like during and afterwards.

Analysis

While long term bonds have rallied in price on Fed support, the recession weighs heavily on companies and municipalities. Credit problems have been simply postponed, while in other situations, especially retail, the pandemic is the last straw and bankruptcies are accelerating.

Long term bonds are unattractive, offering little compensation for default and potential inflation risks.

Investment grade, short term bonds are in such demand as a ‘safe haven’ that it takes a lot of effort to find 1- to 2-year bonds yielding close to a meager 1%.

There has been discussion about yield curve control. The Fed, which controls short term rates, could extend its control to long term rates as well. Frankly, it’s disturbing that the central banks’ (the Fed is a central bank) response to avoiding the consequences of too much borrowing is to continue to enable more borrowing.

So, where does this uncertainty leave us investment-wise?

I don’t have a good feel for this environment. It remains chaotic. My concern is that, in the next six months, it will become clear that the Pandemic’s economic impact will outlast the stimulus. Outlasting the stimulus means that the weight of a halting recovery would pull down stock and real estate prices while unemployment stayed stubbornly high. The election and potential for increased civil unrest add to the uncertainty. Since markets appear to assume this will not be the case, there’s little upside and a whole lot of downside to adding risk.

Essentially, we are in the same place as where we ended last quarter: mostly capital preservation mode waiting for asset prices to drop and offer more potential reward. Areas that I am researching include high yield bonds, hard hit countries (like Mexico) which could ultimately benefit from our Chinese supply chain pullback, and real estate related securities that may offer both yield and a post pandemic inflation hedge.

As always, if you have questions or would like to discuss changes to your portfolio, please call 800-525-8808 or email michael@mcsfwa.com.

1MCS Family Wealth Advisors (MCS) consolidated client returns are dollar-weighted, net of investment management fees unless stated otherwise, include reinvestment of dividends and capital gains and represent all clients with fully discretionary accounts under management for at least one full month in 2020. Individual client returns represent client discretionary accounts under management for the entire period – starting on 12/31/2019 and ending on 06/30/2020. These accounts represent 99% of MCS’s discretionary fee-paying assets under management as of 06/30/2020 and were invested primarily in US stocks and bonds (11% of client assets on 06/30/2020 were invested in tax-exempt municipal bonds). The Stock Index values are based on the S&P 500 Total Return Index, which measures the large capitalization US equity market. The Bond Index values are based on the Barclays Capital US Aggregate Bond Index, which measures the US investment-grade bond market. Index values are for comparison purposes only. The report is for information purposes only and does not consider the specific investment objective, financial situation, or particular needs of any recipient, nor is it to be construed as an offer to sell or solicit investment management or any other services. Past performance is not indicative of future results. 2https://jamanetwork.com/journals/jama/fullarticle/2766651 3https://www.businesswire.com/news/home/20200716005551/en/Lazard-Releases-2020-Global-Healthcare-Lead

Categories

2020 Second Quarter Report & Outlook

The investment strategy I am currently pursuing on your behalf is based on two questions:

As of June 30, 2020 (if MCS clients’ investments were treated as one large portfolio including their cash), on average clients lost 0.25%1, after this year. For comparison purposes, the S&P 500 Total Return Stock Index (S&P 500) fell 3.1%, and the Barclays Aggregate Bond Index gained 6.1%. The range of MCS individual client returns was from a gain of 4.05% to a loss of 6.91%.

Clients with the lowest returns had higher overall allocations to equities because most of their investments were in a pension plan with low equity exposure (so their combined return was better than their non-qualified returns). Clients with the highest returns had exposure to select low-basis stocks that did well or had no equity exposure at all. Overall, MCS client returns were protected by the defensive posture of their portfolios. Short term bonds and low overall exposure to stocks meant that MCS clients remained steady while significant volatility swirled around stock and bond investors.

In last quarter’s newsletter, I talked about chaos. You may have heard the about the Butterfly Effect: by flapping its wings in the just right initial conditions, a butterfly’s slight disturbance of air can create a chain reaction resulting in a tornado. It’s a metaphor that has some basis in fact about the nature of chaotic systems. Small changes in initial conditions can lead to large scale events.

Well, we have just witnessed a Butterfly Effect. The butterfly was an alleged phony $20 bill and a refusal to give up a pack of cigarettes purchased with it. A reactive / escalating set of circumstances lead to the brutal, senseless death of George Floyd, followed by national and global chaos which continue reverberating at high levels of reactivity.

To make things worse, this historic movement for social change is happening smack dab in the middle of a pandemic. Not only has COVID-19 reasserted itself as we reopen, but a race relations crisis that was smoldering for decades has now burst into flame. This has led to a law enforcement crisis, in which people are now questioning whether the warrior police model is counterproductive in many situations. Add to that a contentious national election exacerbated by the collapse of trust among the American people. The ongoing pandemic, experimental policies from the Fed, and the increased odds of a Democratic win likely resulting in higher taxes: it appears there’s plenty of opportunity for more volatility ahead.

What follows is my assessment of our pandemic trajectory, economic trajectory, and the interplay between the two as expressed by the stock and bond markets. In addition, it is important to consider the potential impact of my assessment being wrong.

Below are tables I created as a tool to help me work through these complex issues, and I share them with you so you can see where I’m coming from as I consider the pandemic and the economy. I read a lot of articles from a wide variety of sources. If you have any insights, observations, or information you feel would be relevant, please send me an email.

Analysis

In the US, the virus is currently beating our ability to contain it. An effective, widely available vaccine is being touted as just around the corner. Yet, given the multitude of complexities in executing such a task, a vaccine introduction may look more like our inadequate efforts to implement widespread testing and contact tracing.

I expect a lot of consumer confusion about COVID-19 vaccines given the many trials and sped up development process. It will not take many reports of adverse outcomes to cool people on getting vaccinated, despite the expected benefits. Would it be surprising if “the government can’t tell me to wear a mask” folks morph into “the government can’t tell me to get shots” folks and join the “I don’t trust big pharma / anti-vaccine folks?”

If this sounds too pessimistic, consider the concerns raised in Journal of American Medical Association (JAMA) Viewpoint on May 30, 2020. “Adverse Consequences of Rushing a SARS-CoV-2 Vaccine: Implications for Public Trust2.” The article describes problems with the Salk polio vaccine in 1955:

As speed took precedence over caution, serious mistakes went unreported. One company, Cutter Laboratories, distributed a vaccine so contaminated with live poliovirus that 70,000 children who received that Vaccine developed muscle weakness, 164 were permanently paralyzed, and 10 died.

It goes on to discuss he 1976 swine flu vaccination program, saying:

Poorly conceived, the attempt to vaccinate the US population at breakneck speed failed in virtually every respect. Safety standards deteriorated as one manufacturer produced the incorrect strain. The vaccine tested poorly on children who, depending on the form of vaccine tested, either developed adverse reactions with high fevers and sore arms or did not mount an immune response at all. Reports emerged that the vaccine appeared to cause Guillain-Barré syndrome in a very small number of cases, a finding that remains controversial, but added to the early momentum of the antivaccine movement.

Other challenges to manufacturing a vaccine at an unprecedented scale include:

From Lazard’s Global HealthCare Leaders Study3 released July 16, 2020:

Healthcare industry leaders’ single biggest concern is the availability of an effective vaccine to prevent infections. They are sober about the length of time it will likely take to develop widely available effective vaccines to bring the COVID-19 pandemic under control, and they expect this will not happen until well into 2021, if not later.

To summarize: efforts to develop vaccines will pay-off, but the timing is uncertain. The pandemic is creating breakthroughs and valuable lessons. Yet, it’s a very messy experiment on many levels and it would be naïve to assume the timing and consequences will be only positive for those involved.

Macro-Economic Analysis

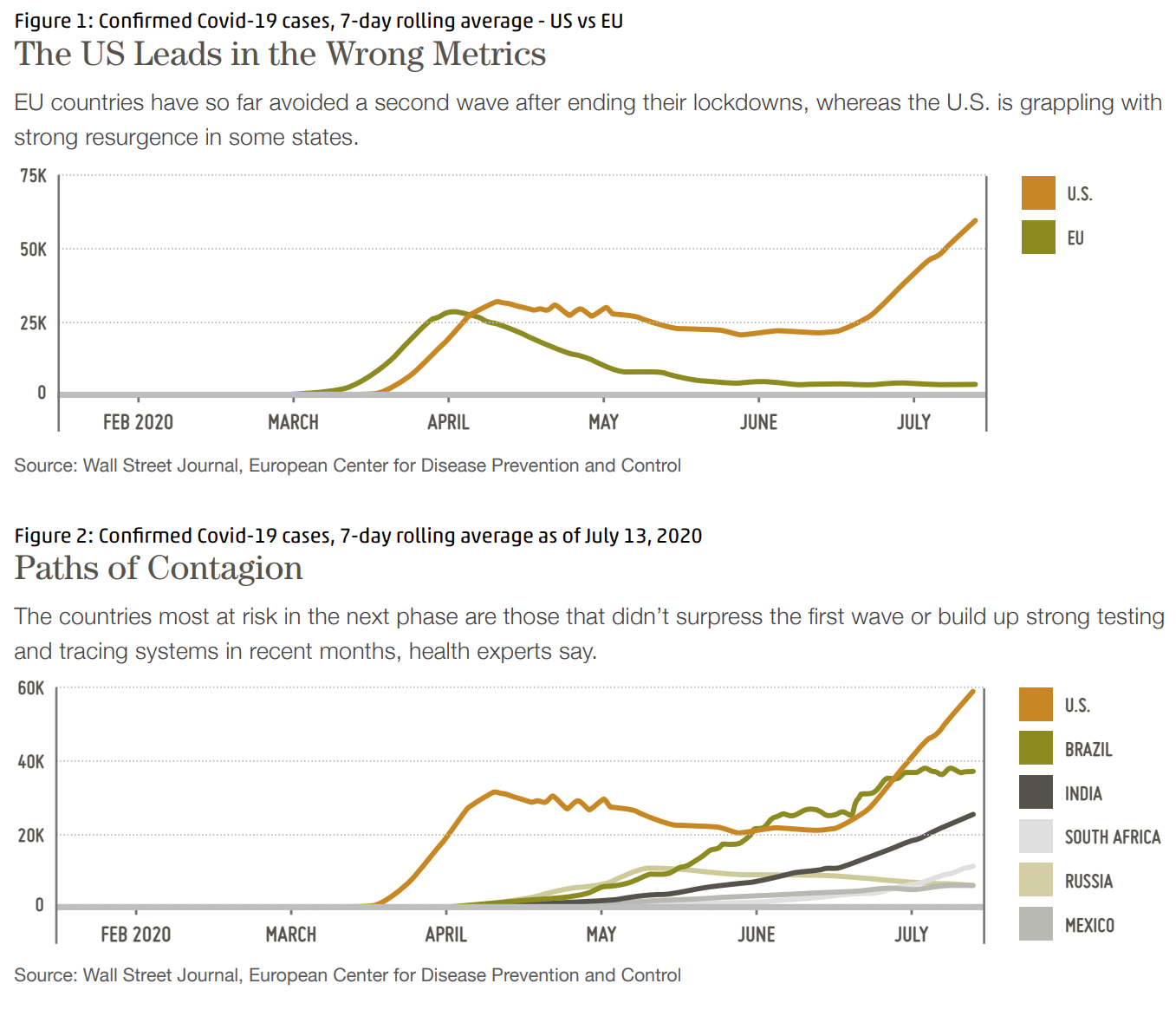

The global pandemic has had a crushing impact on the world economy. Pandemics, like other natural disasters, have varying economic impacts. Wall Street typically dismisses regional natural disasters because the impact on the national economy is muted. However, each disaster has a significant impact on the local economy. Areas hit by severe disasters do not quickly rebound to pre-disaster activity despite federal assistance. The global pandemic qualifies as a severe natural disaster in my mind, which implies a long, uneven global recovery.

Comments

A business and consumer insolvency crisis rapidly unfolded as the pandemic lead to lockdowns (insolvency means not having enough cash on hand to pay bills). The government responded by sending money to individuals and businesses with the hope of bridging the financial problems after lockdowns caused a ‘hard stop’ of economic activity. The hope was that the hard stop would be short lived, but the recovery has faltered as the reopening has created a surge in COVID-19 infections. Regardless of whether economic lockdowns are reinstated, many consumers will not return to their normal economic activity until they feel safe. Yet, safety from the virus may be an illusion. It may settle into humanity as a more deadly version of the flu, where an annual COVID-19 vaccine mitigates the healthcare impact but does not eliminate it.

A counterintuitive possibility is that a promised and ‘soon-to-arrive’ vaccine makes the global economy worse over the short run. A rational response to a soon-to-arrive vaccine for the wealthier over 55 year-olds, who make up a disproportionally large share of leisure consumption, is a self-imposed mini-lockdown while waiting for the miracle vaccine. Yet, it is not hard to imagine the vaccine’s ‘time to delivery’ encountering setbacks which delay the economic rebound.

The pandemic is an invisible tsunami washing over the world. A government cannot stop the destruction of a tsunami simply by offering money and loans to people and businesses in coastal towns. The post-tsunami cleanup takes years and the landscape is permanently altered.

Uncertainty is the Certainty

How have asset prices reacted to a global pandemic and the worst globally synchronized recession in 150 years?

Comments

Because of the unprecedented amount of government money thrown at both the economy and a vaccine, stock prices reflect expectations of a relatively short-lived recession. Frankly I don’t have faith that people who didn’t see the pandemic coming, and who are still learning in real time, will now clearly see how this ends. Of course, it will end, as all pandemics eventually do. The open question is what the US and global economy look like during and afterwards.

Analysis

While long term bonds have rallied in price on Fed support, the recession weighs heavily on companies and municipalities. Credit problems have been simply postponed, while in other situations, especially retail, the pandemic is the last straw and bankruptcies are accelerating.

Long term bonds are unattractive, offering little compensation for default and potential inflation risks.

Investment grade, short term bonds are in such demand as a ‘safe haven’ that it takes a lot of effort to find 1- to 2-year bonds yielding close to a meager 1%.

There has been discussion about yield curve control. The Fed, which controls short term rates, could extend its control to long term rates as well. Frankly, it’s disturbing that the central banks’ (the Fed is a central bank) response to avoiding the consequences of too much borrowing is to continue to enable more borrowing.

So, where does this uncertainty leave us investment-wise?

I don’t have a good feel for this environment. It remains chaotic. My concern is that, in the next six months, it will become clear that the Pandemic’s economic impact will outlast the stimulus. Outlasting the stimulus means that the weight of a halting recovery would pull down stock and real estate prices while unemployment stayed stubbornly high. The election and potential for increased civil unrest add to the uncertainty. Since markets appear to assume this will not be the case, there’s little upside and a whole lot of downside to adding risk.

Essentially, we are in the same place as where we ended last quarter: mostly capital preservation mode waiting for asset prices to drop and offer more potential reward. Areas that I am researching include high yield bonds, hard hit countries (like Mexico) which could ultimately benefit from our Chinese supply chain pullback, and real estate related securities that may offer both yield and a post pandemic inflation hedge.

As always, if you have questions or would like to discuss changes to your portfolio, please call 800-525-8808 or email michael@mcsfwa.com.

1MCS Family Wealth Advisors (MCS) consolidated client returns are dollar-weighted, net of investment management fees unless stated otherwise, include reinvestment of dividends and capital gains and represent all clients with fully discretionary accounts under management for at least one full month in 2020. Individual client returns represent client discretionary accounts under management for the entire period – starting on 12/31/2019 and ending on 06/30/2020. These accounts represent 99% of MCS’s discretionary fee-paying assets under management as of 06/30/2020 and were invested primarily in US stocks and bonds (11% of client assets on 06/30/2020 were invested in tax-exempt municipal bonds). The Stock Index values are based on the S&P 500 Total Return Index, which measures the large capitalization US equity market. The Bond Index values are based on the Barclays Capital US Aggregate Bond Index, which measures the US investment-grade bond market. Index values are for comparison purposes only. The report is for information purposes only and does not consider the specific investment objective, financial situation, or particular needs of any recipient, nor is it to be construed as an offer to sell or solicit investment management or any other services. Past performance is not indicative of future results.

2https://jamanetwork.com/journals/jama/fullarticle/2766651

3https://www.businesswire.com/news/home/20200716005551/en/Lazard-Releases-2020-Global-Healthcare-Lead